4 minutes

How is the fashion industry progressing on the road to eco-responsibility?

In the whole of Europe, the week from 30th May to 5th June is European Sustainable Development Week. Many of the fashion industry’s leading names are staging initiatives in favour of the environment and sustainability, but how eco-responsible really is the fashion industry?

The ‘Pulse of the Fashion Industry’ report, produced by the Copenhagen-based Global Fashion Agenda (GFA) association with consultancy firm Boston Consulting Group (BCG) has some of the answers.

Textile/apparel is the world's second most polluting industry after the oil industry, and has ample room for improving its sustainability performance. Evidence of this comes from the report’s Pulse Score, measuring the performance of textile/apparel companies based on the criteria of the Higg Index, developed by the Sustainable Apparel Coalition.

The textile/apparel sector's overall score is definitely low. Though a 100/100 score is intrinsically unobtainable, the industry’s score is only 38/100. Both the GFA and BCG are however optimistic, as last year, in the report's first edition, the score was 32/100. The share of the companies analysed which haven’t taken any sustainability action has fallen (though it’s still a remarkable 10%), and that of the companies with more than five initiatives under way grew from 56% to 66%. Above all, in 2018 more than half of the companies in question stated that eco-responsible criteria were incorporated in their business strategies. The companies which were active in this respect have on average improved their Pulse Score by 18 points, proof that action yields results.

In actual fact, the level of engagement across the industry is quite uneven. Who are the keenest? European companies first and foremost. In terms of company size, the answer may raise a few eyebrows. While fingers are regularly pointed at the indiscretions of the industry’s giants, it is the bigger groups which are actually more engaged in the issue. The big sportswear names for example are well ahead of the pack with a score of 84/100. A performance explained by their sometimes troubled history in terms of the working conditions in some of their suppliers’ factories, as well as by their efforts to deliver innovative products, which pushes them to tread new ground, notably in the fields of the circular economy and recycled materials.

For the same reason, companies positioned in the entry-level segment and generating more than €8 billion in annual revenue (defined in the report as ‘giant players’) have, on average, a score of 67/100. At the other end of the spectrum, the companies which generate less than €80 million in revenue posted the lowest scores: 20/100 on average for the entry-level segment, and 37/100 for the mid-price segment. The study nevertheless observed that mid-price players, by adopting solutions consistent with the size of their business, have managed to improve significantly. Only the luxury segment recorded the same score for great groups and smaller entities alike: 51/100.

The companies surveyed said they prioritise chiefly design and product development, production processes and, above all, materials. The latter is a crucial area, one in which 89% of companies are keen to make further progress in the next few years. The study highlighted however that, in order to respond to the market's and the consumers’ expectations, short-term innovation in materials will be necessary to furnish new, industry-wide solutions.

The industry’s weakness is the tail end of its products’ life cycle. A few companies do train their styling teams to adopt a circular approach, envisaging from the design phase how products can be recycled, but the majority still has a long way to go. Workshops for garment repairs are beginning to proliferate. The study also observed that improving the recycling of discarded products will still need a few more years. One interesting solution is doubtlessly the use of RFID tags carrying information on the exact composition of the product and the best way to recycle it.

According to analysts however, these changes cannot be implemented piecemeal. Industry players will have to move forward collectively in order to truly step up to the next level.

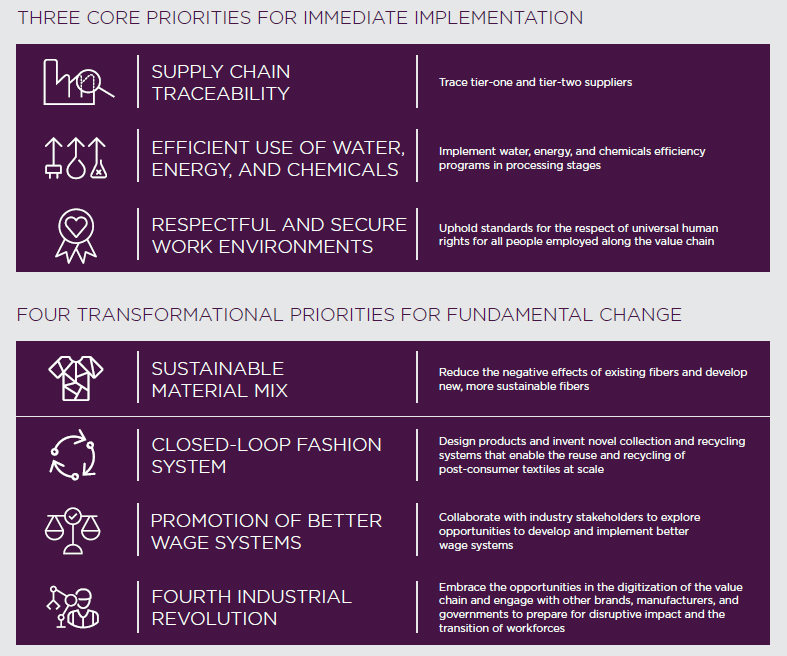

The main challenge eventually identified by the ‘Pulse of the Fashion Industry’ report is that of leading as many companies as possible on the road towards ecological and social change. Also, the report outlined seven key priorities whose implementation is crucial for making progress, appropriate to all companies depending on their current position on these issues. To make comfortable progress, companies need to implement a system for full supply chain traceability, improve the way in which they consume water, energy and chemicals, and uphold and/or demand compliance to standards in terms of working conditions. In a second phase, they should be able to source a responsible mix of sustainable materials, introduce a circular approach to the business, promote improvements in worker remuneration and finally tap the opportunities provided by the electronic and digital revolution.

All of these changes (and investments) need to be incorporated in business strategies. According to the report, those companies which will invest on environmental and social initiatives will earn themselves a ‘bonus’ in operating margin by 2030: rising to the new challenges will be worth the effort.

Copyright © 2024 FashionNetwork.com All rights reserved.